Better-than-expected non-farm payrolls data completely reversed expectations of an interest rate cut, leaving Warsh's first policy meeting in a policy dilemma

ACE Markets' macro research team, combining the latest non-farm payroll data, high-frequency market trends in interest rate derivatives, and consensus from Wall Street institutions, has conducted an in-depth analysis through a cross-asset linkage tracking system: The better-than-expected May employment data has completely shattered any illusions the market had about a Fed rate cut in 2026, with traders now fully pricing in a 25 basis point rate hike this year. The easing measures promised by new Fed Chairman Warsh during his nomination process have been shattered by both economic resilience and sticky inflation. His first policy meeting on June 16-17 will face a dilemma: "adhering to dovish promises damages credibility" versus "shifting to a hawkish stance goes against political expectations." The logic of global asset pricing is undergoing a new round of restructuring.

Non-farm payroll data ignites the market, completely erasing expectations of interest rate cuts.

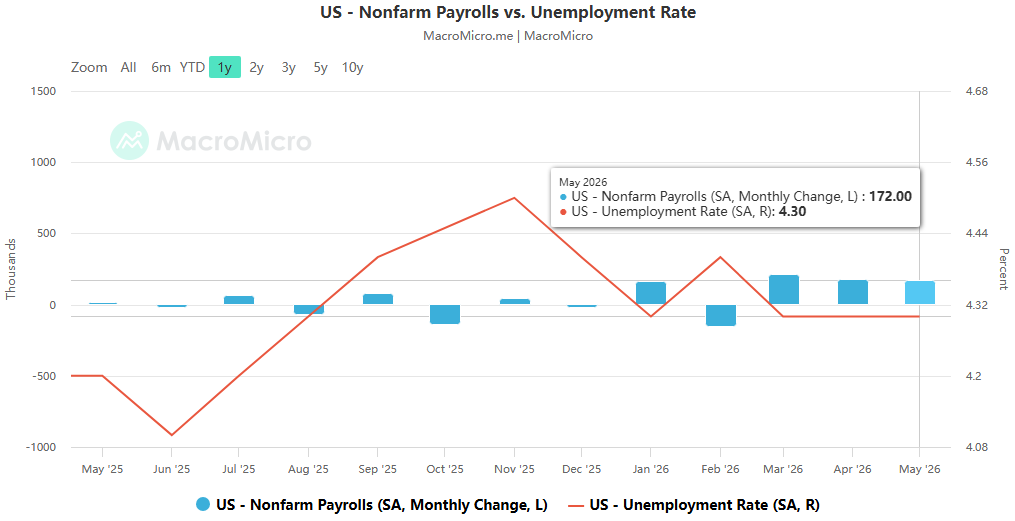

The U.S. Bureau of Labor Statistics released its May non-farm payrolls report on June 4, far exceeding market expectations: 172,000 new jobs were added, with upward revisions of 93,000 jobs for March and April, marking the best three-month job growth in over two years; the unemployment rate remained unchanged at 4.3%, and the resilience of the labor market significantly exceeded market expectations. Following the data release, global financial markets experienced immediate and sharp fluctuations. ACE Markets tracking data showed: U.S. Treasuries faced a concentrated sell-off, with the yield on the 2-year Treasury note, most sensitive to policy, surging 11 basis points to 4.15%, a new high for the year; the 10-year Treasury yield rose 6 basis points to 4.53%, and the 30-year yield once again surpassed the 5% mark; the dollar index strengthened in tandem, and international spot gold plummeted by $100 in a single day, a drop of nearly 2.5%, erasing all gains from the past month.

Interest rate swap market pricing indicates that traders are fully betting on a 25 basis point rate hike by the Federal Reserve in December 2026, with the probability of an October rate hike rising to approximately 60%. This contrasts sharply with the market consensus before the outbreak of the US-Iran conflict at the end of February, which predicted a 75 basis point rate cut throughout the year. ACE Markets, through cross-validation of views from BlackRock, Natixis, and other institutions, believes that a clear consensus has formed in the market: the Fed's next interest rate change will be a rate hike, not a rate cut, and the previous policy logic of relying on weak employment to drive rate cuts has been completely overturned.

It is worth noting that this round of employment recovery exhibits a clear structural characteristic: the increase is mainly concentrated in the leisure and hospitality industry during its seasonal peak and the long-term stable healthcare industry. ACE Markets analysis points out that against the backdrop of the Trump administration's significantly tightened immigration policies and continued constraints on labor supply, even an average monthly increase of only 114,000 jobs is sufficient to keep the unemployment rate stable, fundamentally eliminating the employment-related rationale for the Federal Reserve to cut interest rates.

Federal Reserve officials defect en masse, Warsh faces a crisis of confidence.

With employment and inflation data continuing to exceed expectations, the Federal Reserve's decision-making circle has completed a comprehensive hawkish shift. Fed Governor Waller, who had previously long supported rate cuts, has become a key figure, explicitly withdrawing his inclination towards rate cuts in his latest statement: "If inflation does not fall in the short term, I no longer rule out further rate hikes. The latest employment data demonstrates that the labor market is basically stable and the unemployment rate is low and stable." ACE Markets' tracking of Fed officials' statements reveals that in recent weeks, more than 10 FOMC members have publicly shifted to a hawkish stance, with several officials stating that they cannot support rate cuts given that US inflation continues to be significantly higher than the 2% policy target.

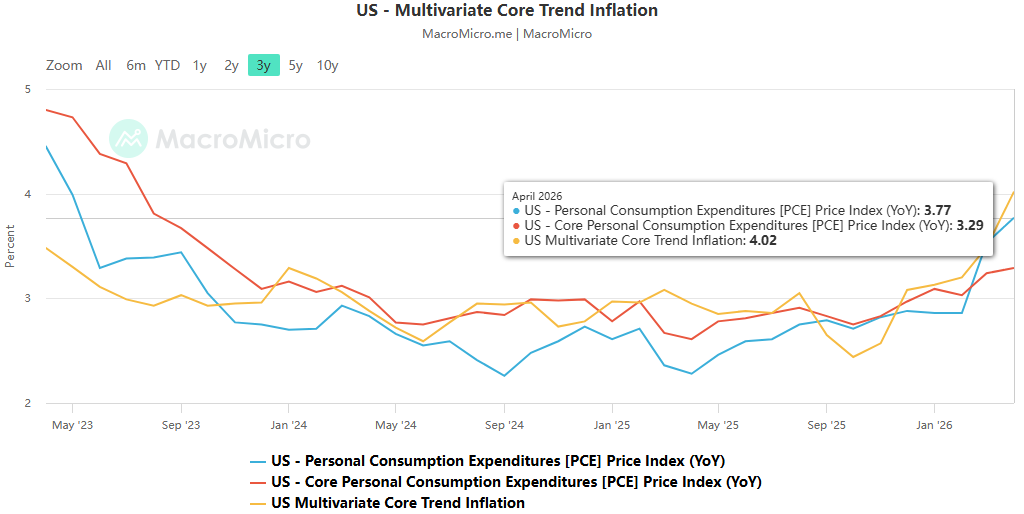

As early as the end of April, three board members voted against raising interest rates, advocating for an immediate increase. Now, with Waller's defection, the hawkish camp has gained an absolute majority within the FOMC. This shift has placed newly appointed Fed Chairman Warsh in an unprecedentedly awkward position. When Warsh officially took office in mid-May, he promised the Fed had ample room to cut interest rates, based on optimistic expectations of Trump's new policies and the widespread adoption of AI technology. However, the actual data has completely deviated from his predictions: US inflation has consistently exceeded the 2% target by more than 1 percentage point, and it is highly likely that it will fail to fall back to the policy target line for the sixth consecutive year; the IMF has even postponed the time when US inflation will return to 2% from mid-2026 to the end of 2027, clearly warning that the risk of upward inflation persists.

ACE Markets' in-depth analysis suggests that Warsh is currently facing a dual crisis of confidence: on the one hand, if he continues to maintain a dovish stance, it will contradict the opinions of most FOMC members and may further damage the Fed's credibility in combating inflation; on the other hand, if he shifts to supporting interest rate hikes, it will directly contradict Trump's core demand for him to be the Fed chairman, exacerbating the policy conflict between the Fed and the White House.

Political maneuvering intensifies, policy uncertainty rises sharply

The complexity of this round of policy maneuvering by the Federal Reserve is compounded by the political factors of the US midterm elections in November. ACE Markets noted that after the release of the non-farm payroll data, the White House quickly interpreted it as an economic achievement of the Trump administration, while simultaneously vehemently denying that strong employment would push up inflation. Trump publicly stated on social media: "Economic growth does not mean inflation! The Fed should not raise rates, and there is still room for rate cuts." White House National Economic Council Director Hassett also urged the Fed to remain on the sidelines and wait for further clarity on the inflation situation.

This divergence between political demands and economic reality further complicates the Federal Reserve's policy decisions. ACE Markets cross-validated the views of Bank of America, Lazard, and other institutions, finding that Wall Street's current baseline expectation for the June FOMC meeting is for interest rates to remain unchanged, but the policy statement will shift significantly towards a hawkish stance, leaving room for future rate hikes. Most institutions believe that as long as the May CPI data released on June 10 does not show an extreme decline, the probability of a Fed rate hike this year will further increase. Institutions such as Beiguang Asset Management point out that the situation in the Strait of Hormuz remains the biggest external variable. If the strait blockade continues and oil prices remain high, energy inflation will further transmit to core prices, forcing the Fed to take action to raise interest rates sooner; conversely, if geopolitical conflicts ease and oil prices fall, the Fed may have more time to observe.

ACE Markets Outlook and Risk Warnings

ACE Markets' macro team believes the next two weeks will be a crucial pricing period for global markets, and investors should pay close attention to two key milestones:

US CPI data on June 10 : The core inflation reading will directly determine the policy tone of the Fed's June interest rate meeting. If the core CPI year-on-year growth rate exceeds 3.5%, the market will quickly price in the possibility of a September rate hike.

The June 16-17 FOMC meeting : Warsh's first press conference will be the highlight, as the market will look for clear signals of a shift in his policy stance and the latest guidance on the path of interest rate hikes this year.

In terms of asset prices, short-term US Treasury yields still have room to rise, the US dollar index will remain strong, and gold may continue to be pressured by rising real interest rates; US stocks will face a dual game of earnings expectations and rising interest rates, and volatility in the highly valued technology sector may intensify.

The content of this article is spontaneously contributed by Internet users, and the views expressed in this article only represent the author himself. This website only provides information storage space services, does not own ownership, and does not assume relevant legal responsibilities.https://www.aneimedzi.cn/html/438.html