Global central bank policies are diverging, with Australia and Japan issuing policy decisions on the same day sending different signals

ACE Markets' Global Central Bank Policy Tracking Team, combining the latest interest rate decisions, high-frequency economic data, and assessments from mainstream institutions, provides an in-depth analysis using a cross-market linkage system: On June 16th, the Reserve Bank of Australia (RBA) and the Bank of Japan (BOJ) announced their monetary policy decisions on the same day, but their policy directions were diametrically opposed. The RBA ended its three-year streak of rate hikes, maintaining its benchmark interest rate at 4.35%, clearly signaling a cooling economy; while the BOJ raised interest rates by 25 basis points to 1.00%, the highest level in 31 years, with combating inflation remaining its core objective. This policy divergence between the two major developed economies' central banks further confirms the unevenness of the global economic recovery and introduces new variables into global asset pricing.

Reserve Bank of Australia: Pause in interest rate hikes implemented, economic slowdown ends aggressive tightening cycle

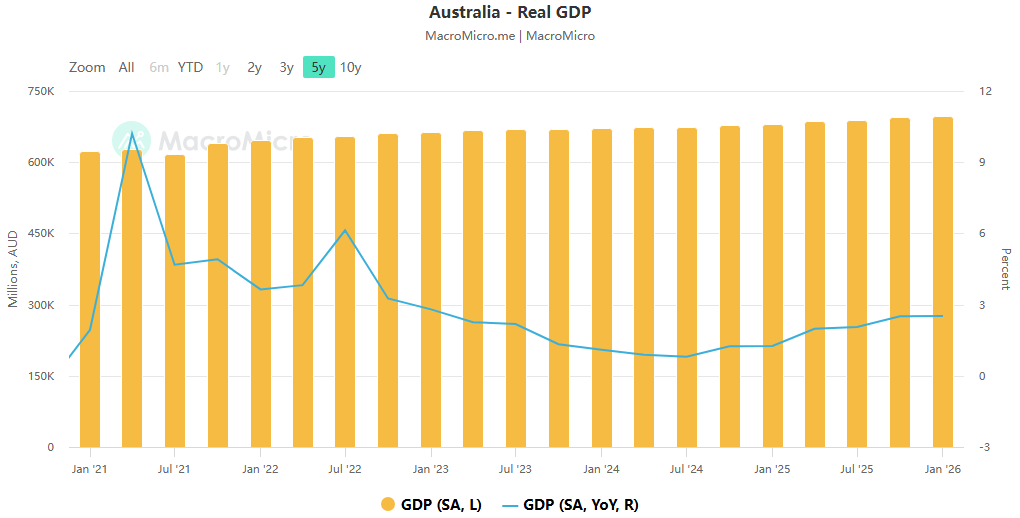

The Reserve Bank of Australia (RBA) announced on Tuesday that it would maintain the official benchmark interest rate at 4.35%, in line with market expectations and officially ending the aggressive tightening cycle of three consecutive rate hikes since 2026. The decision was unanimously approved by the committee. In its statement, the RBA retained the option to raise interest rates, emphasizing that "overall and core inflation remain excessively high, and the cash rate will be raised further if necessary." However, the market and mainstream institutions generally believe that this rate hike cycle has likely peaked. ACE Markets' tracking of macroeconomic data reveals that the core reason for the RBA's pause in rate hikes is the significant cooling of domestic economic activity.

China's real GDP growth in the first quarter was only 0.3% quarter-on-quarter, a significant drop from 0.9% in the fourth quarter of last year; the unemployment rate jumped to 4.5% in May, the highest level since 2021; household spending on non-essential consumer goods has almost stagnated, and the buffer of household savings has been largely exhausted. Fitch Ratings' analysis is highly consistent with ACE Markets' previous assessment: the impact of interest rate hikes in 2026 on consumption will be far greater than in previous cycles, primarily because the cash reserves accumulated by households during the pandemic have been depleted. The impact of interest rate pressure on the household sector is particularly pronounced. ACE Markets' calculations show that, taking a standard new owner-occupied home loan of AUD 745,000 as an example, three interest rate hikes this year have already pushed the monthly payment up from AUD 4,114 to AUD 4,467; if a fourth interest rate hike is initiated, the monthly payment will increase by another AUD 120, further squeezing household consumption capacity.

This is also a key consideration behind the Reserve Bank of Australia's decision to pause policy operations despite inflation not yet meeting its target. Market opinions on the future policy path are clearly diverging. ACE Markets' cross-validation of the views of Australia's four major banks reveals that ANZ, Commonwealth Bank, and National Australia Bank all believe current interest rates have reached their cyclical peak, with a rate-cutting window opening in mid-2027; only Westpac maintains that there will be two more rate hikes in August and September, and that the rate-cutting cycle will not begin until 2028 at the earliest. Financial market pricing indicates that the probability of another rate hike in the next 12 months remains higher than that of a rate cut.

ACE Markets' in-depth analysis suggests that the unemployment rate will be the core variable determining the Reserve Bank of Australia's (RBA) next policy direction. The current unemployment rate of 4.5% has not yet triggered the policy shift threshold, but if subsequent indicators rapidly approach 5% and inflation shows a sustained downward trend, the central bank may open the window for interest rate cuts sooner than expected. Conversely, if the situation in the Middle East continues to push up energy prices, coupled with the expiration of the fuel consumption tax exemption policy, and inflation rebounds again, the possibility of the central bank restarting interest rate hikes cannot be ruled out.

Bank of Japan: Rates raised to 31-year high; 7-1 vote highlights internal divisions.

In stark contrast to the Reserve Bank of Australia's tapering, the Bank of Japan on the same day decided to raise interest rates by 25 basis points by a majority vote of 7 to 1, raising the unsecured overnight call rate to 1.00%, the highest level since 1995, in line with market expectations. This is also the Bank of Japan's first rate hike since 2026.

The resolution statement indicates that the Bank of Japan believes the economy, despite the impact of the Middle East situation and rising oil prices, is maintaining a moderate recovery overall, supported by improvements in corporate profits, employment, and income. However, the price transmission caused by rising oil prices has accelerated, medium- to long-term inflation expectations continue to rise, and there is an upside risk to core CPI exceeding the 2% target. The central bank explicitly stated that it will continue to adjust its policy based on economic, price, and financial conditions, and the window for further interest rate hikes remains open. ACE Markets noted that clear internal disagreements emerged at this meeting.

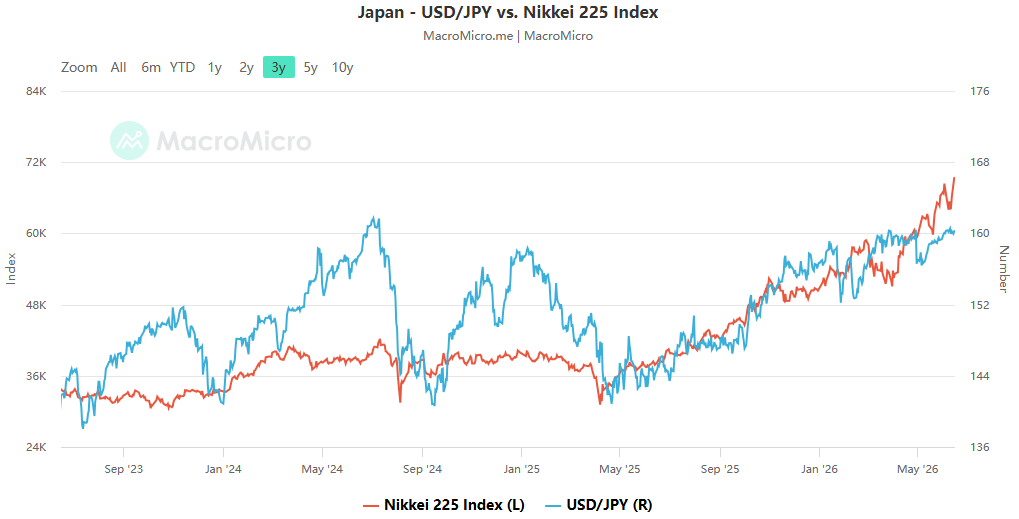

Committee member Toichiro Asada voted against the decision, arguing that the downside risks to production and employment from the Middle East situation outweighed the upside risks to prices, and that maintaining the current policy was more appropriate. This disagreement reflects the Bank of Japan's dilemma between combating inflation and stabilizing growth—addressing energy-driven inflationary pressures while avoiding excessive interest rate hikes that could jeopardize the fragile economic recovery. Market reaction was relatively muted; the yen's exchange rate saw limited short-term fluctuations after the decision was announced, and the Nikkei 225 index fell slightly. ACE Markets analysts believe that the market has fully priced in this rate hike, and investors are more focused on the central bank's future pace of rate increases. Most institutions currently expect the Bank of Japan to raise rates once more this year, but the specific timing will depend on inflation data and the evolution of the Middle East situation.

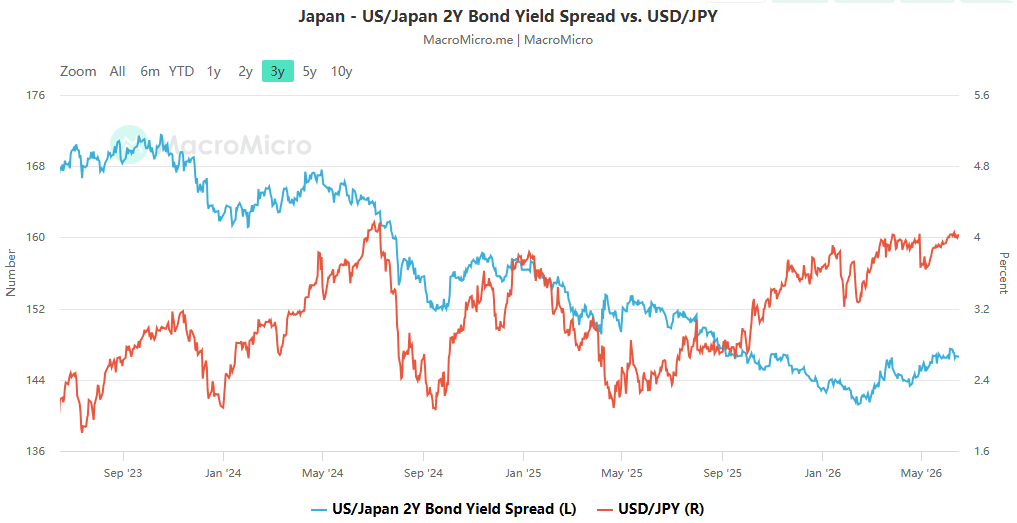

It is worth noting that the Bank of Japan's latest rate hike has further widened the convergence of policy rates with other major central banks, but a significant interest rate differential still exists between it and the Federal Reserve. ACE Markets points out that if the Federal Reserve initiates rate hikes this year, while the Bank of Japan's rate hike pace falls short of expectations, the yen will still face depreciation pressure; conversely, if the Bank of Japan continues to tighten its policy, it may trigger the unwinding of global carry trades, generating spillover effects on global financial markets.

ACE Markets Global Outlook and Risk Warning

ACE Markets' macro team believes that the simultaneous policy decisions by the Reserve Bank of Australia and the Bank of Japan signify a further widening of the divergence in global central bank policies. Against the backdrop of sticky inflation and economic growth pressures, major central banks will adopt differentiated policy paths based on their respective national economic fundamentals, which will increase the volatility of global asset prices.

Investors need to pay close attention to two key risks:

Energy price volatility risk : The situation in the Middle East remains a core variable affecting global inflation. If the blockade of the Strait of Hormuz continues and oil prices rise further, it may force more central banks to postpone interest rate cuts or restart interest rate hikes.

Policy spillover effects : The Bank of Japan's continued interest rate hikes may trigger a restructuring of global capital flows, especially the unwinding of carry trades, which could impact assets such as US Treasury bonds and US stocks.

This article provides macroeconomic analysis and information interpretation for reference only and does not constitute any investment advice, trading strategy, or operational basis. Market conditions are constantly changing, and various policy, geopolitical, and data variables may cause asset price fluctuations. All investment decisions and any resulting profits or losses are the sole responsibility of the investor.

The content of this article is spontaneously contributed by Internet users, and the views expressed in this article only represent the author himself. This website only provides information storage space services, does not own ownership, and does not assume relevant legal responsibilities.https://www.aneimedzi.cn/html/444.html